Income Tax: The Indian Income Tax system is intricate as it covers important aspects of the economy. There are various concepts in Income Tax and one concept that is often confusing for taxpayers is the difference between Tax Deducted at Source or TDS and Tax Collected at Source or TCS.

Let us understand both concepts in detail.

Read More: Calculate Your Income Tax Under Old And New Regimes In Govt’s IT Calculator; Here’s How To Use It

Income Tax: What is Tax Deducted at Source or TDS?

TDS is the amount deducted from payments made for specified services. The source can be professional fees, contract payments, commission and royalty payments and so on. TDS can also be applied to certain types of investment including interest earned from fixed deposits and other deposits in banks, post offices, and so on.

The concept of TDS was introduced with the aim to collect tax from the source of income.

Income Tax: How does TDS work?

According to the concept of TDS, a person or an institute (deductor) who is liable to make payment for service shall deduct tax at source and remit the same into the account of the Central Government.

This TDS amount can be claimed back on the basis of Form 26AS for the TDS certificate issued by the deductor.

Income Tax: TDS tax slab

Read More: Is Income On Fixed Deposits Taxable In India?

| Section | Nature of transaction | Threshold Limit (Rs) | TDS Rate |

| 192 | Payment of salary | Basic exemption limit of employee | Normal Slab Rates |

| 192A | Premature withdrawal from EPF | 50,000 | 10% |

| 193 | Interest on securities | Debentures- 5,000 8% Savings (Taxable) Bonds 2003 or 7.75% Savings (Taxable) Bonds 2018- 10,000 Other securities- No limit | 10% |

| 194 | Payment of any dividend | 5,000 | 10% |

| 194A | Interest from other than interest from securities (from deposits with banks/post office/co-operative society) | Senior Citizens- 50,000 Others- 40,000 | 10% |

| 194A | Interest from other than interest on securities u/s 193 and interest from banks/post office/co-operative society. For e.g., interest from friends and relatives | 5,000 | 10% |

| 194B | Income from lottery winnings, card games, crossword puzzles, and other games of any type | 10,000 | 30% |

| 194BB | Income from horse race winnings | 10,000 | 30% |

| 194C | Payment to contractor/sub-contractor:- Individuals/HUF | Single transaction- 30,000 Aggregate transactions- 1,00,000 | 1% |

| 194C | Payment to contractor/sub-contractor:- Other than Individuals/HUF | Single transaction- 30,000 Aggregate transactions- 1,00,000 | 2% |

| 194D | Insurance commission to domestic companies | 15,000 | 10% |

| 194D | Insurance commission to other than companies | 15,000 | 5% |

| 194DA | Income for the insurance pay-out, while payment of any sum in respect of a life insurance policy. | 1,00,000 | 5% |

| 194E | Payment to non-resident sportsmen/sports association | No limit | 20% |

| 194EE | Payment of amount standing to the credit of a person under National Savings Scheme (NSS) | 2,500 | 10% |

| 194F | Payment for the repurchase of the unit by Unit Trust of India (UTI) or a Mutual Fund | No limit | 20% |

| 194G | Payments, commission, etc., on the sale of lottery tickets | 15,000 | 5% |

| 194H | Commission or brokerage | 15,000 | 5% |

| 194-I | Rent onplant and machinery | 2,40,000 | 2% |

| 194-I | Rent onland/building/furniture/fitting | 2,40,000 | 10% |

| 194-IA | Payment in consideration of transfer of certain immovable property other than agricultural land. | 50,00,000 | 1% |

| 194-IB | Rent payment by an individual or HUF not covered u/s. 194-I | 50,000 per month | 5% |

| 194-IC | Payment under Joint Development Agreements (JDA) to Individual/HUF | No limit | 10 |

| 194J | Any sum paid by way of fee for professional services | 30,000 | 10% |

| 194J | Any sum paid by way of remuneration/fee/commission to a director | 30,000 | 10% |

| 194J | Any sum paid for not carrying out any activity concerning any business; | 30,000 | 10% |

| 194J | Any sum paid for not sharing any know-how, patent, copyright, etc. | 30,000 | 10% |

| 194J | Any sum paid as a fee for technical services | 30,000 | 2% |

| 194J | Any sum paid by way of royalty towards the sale or distribution, or exhibition of cinematographic films | 30,000 | 2% |

| 194J | Any sum paid as fees for technical services, but the payee is engaged in the business of operation of the call center. | 30,000 | 2% |

| 194K | Payment of any income for units of a mutual fund, for example, dividend | No limit | 10% |

| 194LA | Payment in respect of compensation on acquiring certain immovable property | 2,50,000 | 10% |

| 194LB | Payment of interest on infrastructure debt fund to Non-Resident | No limit | 5% |

| 194LC | Payment of interest for the loan borrowed in foreign currency by an Indian company or business trust against loan agreement or the issue of long-term bonds | No limit | 5% |

| 194LC | Payment of interest for the loan borrowed in foreign currency by an Indian company or business trust against the issue of long-term bonds listed in IFSC | No limit | 4% |

| 194LD | Payment of interest on bond (rupee-denominated) to FII or a QFI | No limit | 5% |

| 194LBA(1) | Certain income distributed by a business trust to its unitholder | No limit | 10% |

| 194LBA(2) | Interest income of a business trust from SPV distribution to its unitholders | No limit | 5% |

| 194LBA(2) | Dividend income of a business trust from SPV, in which it holds the entire share capital exempt the capital held by the government, and distribution to its unitholders | No limit | 10% |

| 194LBA(3) | Rental income payment of assets owned by the business trust to the unitholders of such business trust | No limit | 30% |

| 194LBA(3) | Rental income payment of assets owned by the business trust to the unitholders of such business trust | No limit | 40% |

| 194LBB | Certain income paid to a unitholder in respect of units of an investment fund | No limit | 10% |

| 194LBB | Certain income paid to a unitholder in respect of units of an investment fund | No limit | 40% |

| 194LBC | Income from investment in securitisation fund received to an individual and HUF | No limit | 25% |

| 194LBC | Income from investment in securitisation fund received to a domestic company | No limit | 10% |

| 194LBC | Income from investment in securitisation fund received to a foreign company | No limit | 40% |

| 194LBC | Income from investment in securitisation fund received to NRI | No limit | 10% |

| 194M | Certain payments by Individual/HUF not liable to deduct TDS under Section 194C, 194H, and 194J | 50,00,000 | 5% |

| 194N | Cash withdrawal exceeding a certain amount | 1 crore | 2% |

| 194N | Cash withdrawal in case person not filing ITR for last three years and the original ITR filing due date expired | -20 lakh to 1 crore -1 crore | 2% 5% |

| 194O | Payment for the sale of goods or provision of services by the e-commerce operator through its digital or electronic facility or platform. | 5,00,000 | 1% |

| 194P | Payment of pension or interest to specified senior citizens of age 75 years or more | Basic exemption limit of senior citizens or super senior citizens | Normal tax slab rates |

| 194Q | Payments for the purchase of goods | 50,00,000 | 0.10% |

| 194R | Perquisite or benefit to a business or profession | 20,000 | 10% |

| 194S | TDS on the transfer of virtual digital assets | Specified Persons- 50,000 Others- 10,000 | 1% |

Income Tax: What is Tax Collected at Source or TCS?

A tax collected by a seller or a service provider from the buyer at the time of sale of goods or provisions of services is TCS. It is applicable to certain goods and services such as alcohol, coal, toll plaza, etc.

It is applicable on amounts involved in the transaction more than Rs 2 lakhs. The TCS rate varies from 0.1 per cent to 10 per cent depending upon the type of goods or services.

Read More: Income Tax: Know the new rules for NRIs – Explained, non resident indians

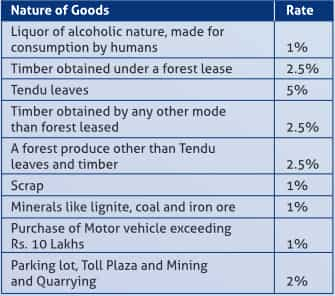

Income Tax: TCS slab

Income Tax: TCS Vs TDS

| Factors | TDS | TCS |

| Applicability | Applicable on the sell of goods and services | Applicable to income |

| Liability | Deductor has to collect the tax | The seller has to collect tax on the sale ofspecified goods and services |

| Rate of taxation | Higher than TCS | Lower than TDS |

| Tax Payment | The amount is deducted from thepayer’s account before paymentand deposited with the government | The amount collected is paid directlyto the government |

| Filing Return | No filling required | Filing as per Income Tax Act |

| Return on excess tax paid | the excess amount can be claimed as a refund | the excess amount cannot be refunded |