Lenders use credit scores to assess the risk of lending money to you, and they use this information to determine the interest rate they will charge you on the home loan.

One of the crucial factors while applying for any loan is your credit score. It helps determine whether you will be approved for a home loan and, if so, at what interest rate. Lenders use credit scores to assess the risk of lending money to you, and they use this information to determine the interest rate they will charge you on the home loan.

What is Credit Score?

A credit score is a three-digit number that explains your entire credit history. The value of a credit score typically ranges between 300 and 900. Your credit score is prepared based on your credit history. It includes all secured or unsecured loans and any other debts you may have.

Read More: LIC Kanyadan Policy: Pay Rs 121, get Rs 27 lakh in bumper returns

A higher credit score generally indicates that you are a lower-risk borrower, and, as a result, you may be offered a lower interest rate. On the other hand, a lower credit score can result in either a denial of the loan or a higher interest rate, which can make your monthly mortgage payments more expensive. Therefore, it’s essential to maintain a good credit score, as it can significantly impact the cost of borrowing.

What Is Good Credit Score?

Often people with poor credit scores need help in getting their loans approved. A score of 650 and above can help you get a loan. Whereas if your score is above 750, you will get the loan quicker, and the interest rates will also be cheaper. Lenders give preference to those customers who have high credit scores. The reason is simple, a good credit score assures lenders that default is unlikely.

How is My Score Used for Home Loans?

When you apply for a home loan, the bank will obtain your credit score from credit agencies and check your repayment history along with other things such as your income, employment etc. Banks give preference to clean credit records as it helps them disburse loans more efficiently by avoiding taking on risky customers, thereby reducing defaults.

Credit Score-Based Home Loans

The importance of credit score is such that some banks offer interest rates on home loans based on the applicant’s score. So, people with high scores are given preference in lending at cheaper rates than what is available in the market. If your credit score is also on the higher side, you can borrow at cheaper rates which can help you save on the total interest outgo on your home loan.

It is advisable to check your eligibility and repayment capacity before borrowing. If you fail to repay your home loan on time, the penalties are high enough to spoil your credit records. Also, if you default on your home loan, your property can be auctioned to recover the debts. A financial discipline is required when borrowing for long terms, like 15-20 years.

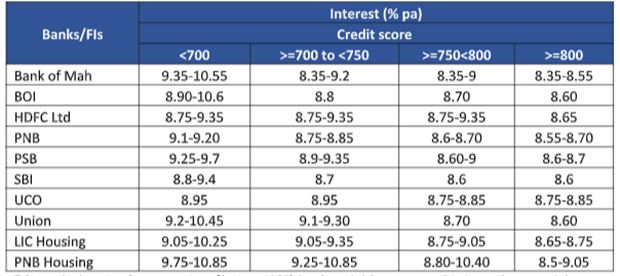

Here are some banks offering home loans based on your credit score. You can compare and take a call based on your requirements and credit score.

Home loan interest rate corresponding to different level of credit score

Note: The table consists of home loan interest rates of banks and NBFCs that shows their home loan rate linked to credit score on their website. Interest rate is indicative and in actual situation the rate may vary depending on various factors and bank’s T&C. Data as on 07 Feb 2023.