The real estate activity in Tier 2 cities is fast catching up with that of Tier 1 cities.

Ahmedabad, Vadodara, Nashik, Gandhi Nagar and Jaipur have taken up the top five ranks among Tier-II cities in growth of residential property market on the back of rapid urbanisation, industrialisation and growth of IT industry, according to a report by PropEquity.

The report, titled “Tier-II: Residential Overview”, states that there has been a remarkable jump in both absorption as well as supply of quality residential properties in various price brackets in these cities. The report has tracked performance of the residential segment of the real estate sector in various Tier-II cities from FY 2017-18 to FY 2021-22.

“The real estate activity in Tier 2 cities is fast catching up with that of Tier 1 cities. Interestingly, Ahmedabad’s residential real estate market size of Rs 83,390 crore has outshone some of the Tier 1 cities like Chennai and Kolkata with market sizes of Rs 52,554 crore and Rs 38,440 crore, respectively, at the end of fiscal year 2021-22. Although it is also interesting to observe that the market share of Tier-I cities is about 4x times the share of Tier-II cities in the last five fiscal years,” said Samir Jasuja, Founder and Managing Director at PropEquity.

“Post COVID lockdowns, Tier 2 cities have been witnessing new job creation at a decent rate and many tech and other sector companies are encouraging work from home for their employees for at least the next couple of years. This has led to scenarios where Tier 2 city housing projects are getting great traction due to their attractive pricing and potential for a higher upside in terms of investments,” said Abhishiekh Andlay, Founder, Andlay Estates.

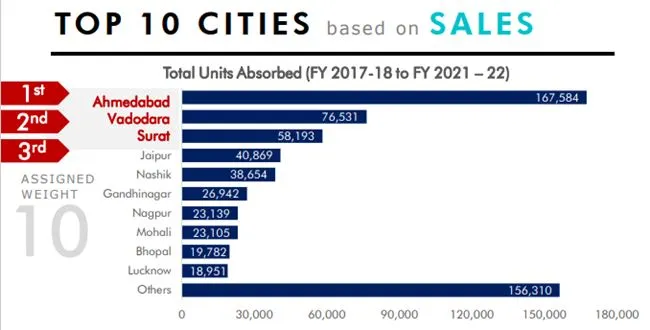

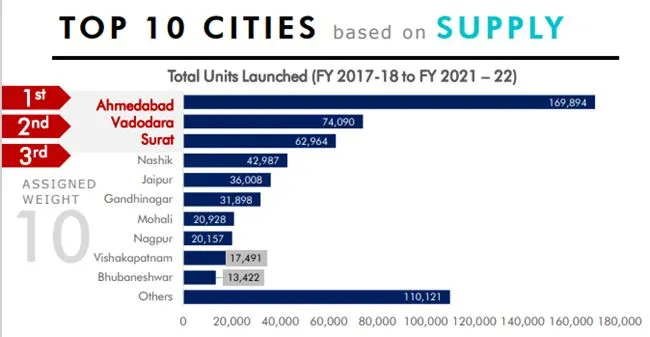

Ahmedabad – Sales of homes in Ahmedabad stood at 39,046 units in fiscal year 2021-22, a growth of 26% as compared to financial year 2020-2021. When compared to fiscal 2017-18, a growth of 32% was witnessed in the city. The supply of homes in Ahmedabad stood at 39,195 units in financial year 2021-22, a growth of 14% as against fiscal year 2020-2021.

The unsold stock of homes stood at 62,047 units at the end of fiscal year 2021-22, almost the same as fiscal 2020-2021. The inventory overhang will take about 24 months to clear at the current rate of absorption of houses.

Vadodra – Second ranked Vadodara witnessed a growth of 25% in sales of homes at 17,285 units in fiscal 2021-22 as compared to the previous fiscal. When compared to the financial year 2017-18, a jump of 20% was seen. The supply of new homes stood at 15,046 units in fiscal 2021-22, an increase of 9% as against the previous financial year.

The inventory of homes in Vadodara stood at 27,070 units at the end of fiscal 2021-222, a decline of 8% when compared to the previous financial year. It will take 19 months to clear at the current rate of sales.

Nashik – Third-ranked Nashik witnessed sales of 10,806 units in fiscal 2021-22, a growth of 15% on year-on-year basis. New supply of homes in Nashik stood at 13,037 units in 2021-22 fiscal, a whopping growth of 68% as compared to the previous fiscal. The inventory of houses in Nashik stood at 15,837 units at the end of 2021-22, a growth of 17% when compared to the previous financial year. It will take 17 months to clear at the current rate of sales.

Gandhinagar – Fourth-ranked Gandhi Nagar saw sales of 7,650 units in fiscal 2021-22, a growth of 10% as compared to the previous fiscal. New supply of homes in Gandhi Nagar stood at 6,361 units in the financial year 2021-22, a drop of 30% on a year-on-year basis.

Jaipur – Fifth-ranked Jaipur saw sales of 7,676 units in fiscal 2021-22, a whopping growth of 42% as compared to the previous fiscal. New supply of homes in Jaipur stood at 7,022 units in the financial year 2021-22, a massive increase of 78% on a year-on-year basis.

The inventory of homes in Jaipur stood at 14,529 units at the end of fiscal 2021-22, a marginal dip of 4% when compared to the previous fiscal. It will take 23 months to clear at the current rate of sales.