GST on Rent: The Goods and Services Tax (GST) on rent has been implemented with effect from 18 July. But the GST will apply only in certain conditions and not in all cases. The government recently withdrew exemption on renting of residential dwelling to business entities (registered) after the recommendations of the 47th GST Council Meeting.

Kbp Advisory and Tax Consultancy Pvt Limited, a Noida-based tax advisory firms breaks its down for us where taxes are applicable and where they are not.

Read More:-EXPLAINED: Rising Interest Rates – How Will It Impact Your EMIs, Investments?

GST on Rent on Property: Different Permutation and Combinations:

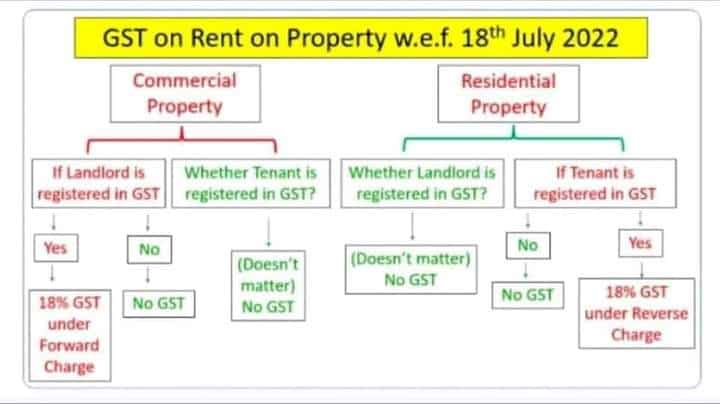

1) Commercial Property:

a – If landlord is registered under GST, there will be 18 per cent GST under forward charge basis.

b – If landlord is not registered under GST, there is no GST on commercial property.

c – Whether tenant is registered under GST – Does not matter and no GST is applicable.

2) Residential Property:

a – If landlord is registered under GST – Does not matter and no GST is applicable.

b – If tenant is registered under GST, no GST when it is rented to private person or for personal use.

c – 18 per cent GST on renting of residential unit if it is rented to business entity.

See Chart

The government also came out with a fact check after certain sections of media reported 18 per cent GST on renting of residential property.

The government has further clarified that there will be no GST on renting of residential properties if proprietor or partner of firm rents residence for personal use.