In today’s edition of Money Guru, hosted by Zee Business’ Swati Raina, Prathiba Girish, founder of Finwise Personal Finance Solutions, will decode the two schemes.

Money Guru: Retirement planning at the early stage of career is very crucial. Therefore, charting the right financial strategy is a must to generate a handsome corpus when you retire.

There are multiple schemes available today offering lucrative returns. But the most popular among them are Public Provident Fund (PPF) and National Pension System (NPS). Both the schemes are backed by the Central government. The basic difference between PPF and NPS is that the former offers a fixed return and the latter is linked to the market return.

Read More: Bank of Baroda Raises Fixed Deposit Interest Rates; Know Latest FD Rates

For those wondering which is the best retirement tool, Zee Business will tell the benefits of investing in both schemes and reap the maximum benefits. In today’s edition of Money Guru, hosted by Zee Business’ Swati Raina, Prathiba Girish, founder of Finwise Personal Finance Solutions, will decode the two schemes.

PPF is often considered to be a scheme that offers risk-free guaranteed returns. As a long-term investment tool, it can be used by all including salaried, professionals, home-makers, self-employed and even those who are not part of the workforce. It is a debt investment tool and a salaried person can claim for tax waiver under section 80c of the IT Act, 1961. Under this scheme, the amount invested, interest earned and maturity are tax exempt.

NPS, on the other hand, launched in 2004, allows the subscribers to make contributions towards planned savings thereby securing the future in the form of a pension. It allows you to invest in schemes that combine equity with corporate and government debt securities. The NPS also provides tax deductions under Section 80 of the Income Tax Act.

Read More: DBS Bank Raises Fixed Deposit Interest Rates; Know Latest FD Rates

She said that when the investment horizon is long, “we often consider securities”. In PPF, you get a guaranteed return and also there’s a lock in period of 15 years.

“When you invest in NPS, a large portion of your investment goes into equities because it can generate a huge return. In NPS, you get 60% of the accumulated money while 40% is allocated for buying annuity at retirement,” she said.

She said that but for the corporate employees who retire early, they have to allocate 80% of the investment to the annuity.

Stating that “risk and return are two sides of a coin”, she said that in NPS you can claim tax deductions up to Rs 50,000 under 80CCD. “This is an extra tax rebate if your investment horizon is long.”

PF vs NPS

– PPF NPS

Maturity 15 years 70 years of age

For whom Self/ Minor 18-60 years of age

Maximum investment Rs 1.5 lakh No limit

Tax Benefit Rs 1.5 lakh Rs 50,000 additional

Return 7.1% 11% (estimated)

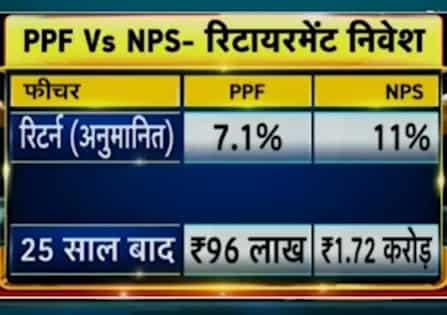

PPF vs NPS (Retirement Investment)

– PPF NPS

Investment amount Rs 1.5 lakh Rs 1.5 lakh

Investment period 25 years 25 years

Return 7.1% 11% (estimated)

After 25 years Rs 96 lakh Rs 1.72 crore