People having high salaries not only need to pay tax on salary income, but also on investment income as well as on rental and other unearned income etc.

People having high salaries not only need to pay tax on salary income, but also on the returns they generate through investments in most of the financial instruments as well as investments in properties generating rental income and on such other unearned incomes.

So, how may they reduce the tax liabilities while generating additional income?

While a physically fit salaried person can’t save much tax on salary income after availing the deductions u/s 80C, 80D, 80CCD(3), etc, they may avail deductions u/s 80C and under few other sections of the Income Tax Act again by forming an entity – called Hindu Undivided Family (HUF) by making investments through HUF and receiving the incomes other than salary through it.

Dr. Suresh Surana, Founder, RSM India explains the tax benefits of investing through HUF instead of investing in an individual’s name.

A Hindu Undivided Family (HUF) is assessed as a separate entity for the purpose of assessment under the Income Tax Act, 1961 (hereinafter referred to as ‘the IT Act’) and further enjoys threshold exemption of income of Rs 2.5 lakh as well as can claim deductions under section 80C to 80U and exemptions under section 54, 54F etc. Such threshold exemptions and deductions are in addition to those enjoyed by the individual. Thus, making investments through HUF may help to reduce tax liability to certain extent.

Read more: Income Tax Return Filing: Here’s how to verify ITR other than Aadhaar

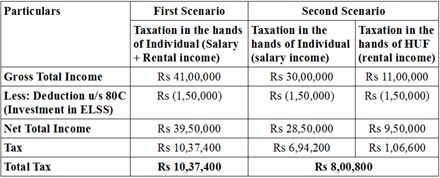

For the purpose of understanding let’s assume that,

a. In the first scenario, Mr. A has a Salary Income of Rs 30 lakh and Rental Income of Rs 11 lakh (net of standard deduction of 30 per cent) from a house property along with investments in ELSS of Rs 3 lakh.

b. in the second scenario, Mr. A has salary income of Rs 30 lakh and has an ELSS of Rs 1.5 lakh and his HUF has rental income of say Rs 11 lakh (net of standard deduction of 30 per cent) and in the HUF investments of Rs 1.5 lakh is made in ELSS as well.

In the above scenarios, the indicative tax levied would be as follows:

Read more: CBDT chief gives key reasons behind robust direct tax collections

Thus, there is a significant tax savings of Rs 2,36,600 by way of HUF.

Is there any regulatory hardship in investing through HUF compared to individual investments?

“There are no major hardships except that as HUF is assessed as a separate entity, creation of HUF would require maintenance of a separate bank account in the name of such HUF, application of PAN for the HUF, etc. Moreover, once the investments are made in the name of the HUF, all the coparceners of such HUF would acquire a right in the properties / assets owned by the HUF,” said Dr. Surana.