This will lead to expansion of the credit market and credit- starved segments will get access at a right rate.

India’s second COVID wave is abating, the lockdowns have been lifted yet the economy is in uncharted territory, humming tentatively as a third wave lurks threateningly in the background. The tentative recovery needs the momentum of reforms to roar. An anemic post-pandemic growth will not do, fundamental reforms are needed to create the momentum.

Earlier, reforms used to be “important”; with a limping economy now threatening to go into a comatose state, reforms need to be undertaken with a never-before sense of urgency.

Some sectors have been irreversibly changed, some things will never be the same again. The pandemic has reduced household savings and may have even changed the outlook towards discretionary spending in the mid-term. The loss of the savings cushion is due to cut in wages, loss of jobs, or in the worst case, the disappearance of certain jobs. Many families have lost their primary breadwinners; the loss of savings due to healthcare costs will also reduce their consumption in the mid-term.

Despite interest rates being at a 20-year low, our large corporations have deleveraged their balance sheets and reduced their debt. According to an analysis of India’s top 15 industrial sectors by our largest bank, the State Bank of India, nearly $22.8 billion worth of debt was pared down last year. Traditional industries like steel, fertilizers, mining, mineral products and textiles have reduced their debt by more than Rs 1.5 trillion last year, and this trend is continuing this year.

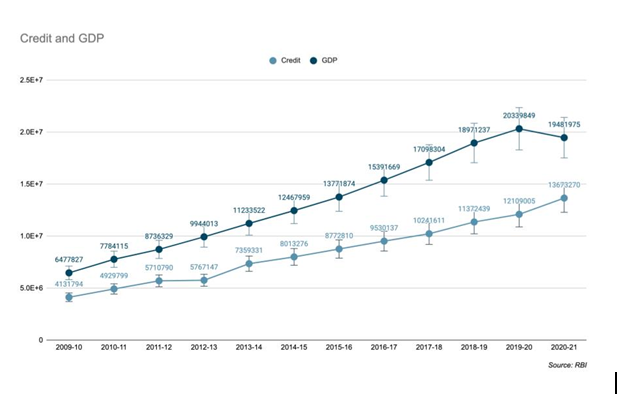

These are not good signals for private capital formation and it is likely to push economic growth downwards. Credit and economic growth feed upon each other. Economists call it bidirectional causality meaning one affects the other’s growth. To boost grassroots economic activity in post-COVID India when corporate revenues have been squeezed and growth is uncertain, credit especially at a competitive rate should now be targeted at the small and medium enterprises, India’s largest employers.

SMALL ENTERPRISES, BIG CRUNCH

The traditional banks have always shied away from micro, small and medium enterprises or MSMEs because of risk aversion and the sheer challenge of managing the unwieldy numbers of small borrowers, a task that such banks are ill-equipped for. This risk aversion combined with the slowdown of credit offtake means that the revival will be slow and protracted. Though the government has launched a credit guarantee scheme to revive the credit to the sector. It is not going to be sufficient as NPA-burdened banks are always wary of lending to this sector.

The uncertainty in several sectors means that companies are going into withdrawal mode. A few are still ‘talking’ about expansion or investment but there is no sign of an upsurge in the investment cycle. The policy makers cannot continue to play a tweak here or there—the reforms have to be structural.

One structural reform needed is in the financial system. A banking system burdened by non-performing assets (NPAs) and aversion to risk is working at less than optimum level. Several sectors are credit starved and several others need lower cost of capital. The regulator has been shying away from risk; it does not want new players to enter as it is not sure whether it will be able to handle them. The regulator has burdened the non-banking sectors with so many regulations that they have hardly any freedom to function. Deposit mobilization is so heavily controlled that it goes into the coffers of NPA-burdened banks where it is frittered away on existing borrowers.

Regulators do not differentiate between a large NBFC and a small NBFC. While a large non-banking financial company or NBFC can be a systemic risk a smaller NBFC is unlikely to be one. NBFCs are also essential for ensuring credit reaches specific regions or segments. Hence regulations should tighten with size, say above Rs 50,000 crore, and for a group. The flexibility for smaller NBFCs may ease up the credit crunch for smaller companies.

DIGITAL BANKS ARE THE FUTURE

Of course, the most important reform is relaxing the logjam in the banking sector by allowing new banks to come in. The experiment with Small Finance Banks (SFB) is ongoing but their impact on the economy is limited at the moment. It is time for the regulator to look at digital banks and address the issue of branchless banking.

It does not make sense for the regulator to shy away from the biggest global trend—digital banks—that is shaping banking, due to unresolved issues. Branchless banking is a contentious issue as traditional banks are opposing it for newcomers.

Banks that are saddled with branches bear fixed establishment costs, salaries of employees, rentals and other costs. All these costs are a large part of the total costs. Moreover, Indian public sector banks have opened hundreds of branches which are not financially viable. Most of these branches have been opened in rural and backward areas under regulatory duress. Hence they do not want new competitors coming in with branchless banking in the form of digital banks. The regulator is also more concerned about the status-quo and is chary of a disruption.

COVID has further exacerbated the financial viability of branches as customers have moved most of their transactions online. Once comfortable with banking or moving transactions online it is the rare few who will come back to interacting at the branch. The digitally deprived will still need to be at branches and they are more likely to be in backward areas or among the urban disadvantaged.

The regulator has to address the emerging scenario of branchless banking. Moreover, it also has to consider that the lack of digital banking prevents the economy from benefiting from lower cost of capital. The entry of digital banks will lead to expansion of the credit market and credit-starved segments will get access at a right rate.

This is a structural reform that is needed now as it will force the banking sector to improve its efficiency. And any improvement in efficiency in the financial sector of the economy has a salubrious impact on the whole economy.